Office Closing

July 1, 2019 by

Brya Insurance will be closed on Tuesday July 2nd 2019 for the funeral of agency co-founder Denny Brya. Denny and his brother Frank built the agency from scratch in 1955. His obituary may be found here https://www.news-gazette.com/obituaries/dennis-brya/article_4d2b957e-9afc-11e9-9a67-5cb9017bdf7c.html .

On a personal note, thank you Dad for being a fantastic mentor and showing us how to work for and value our many loyal customers.

Denny Brya

“Wait a minute, REALLY?”

May 22, 2014 by

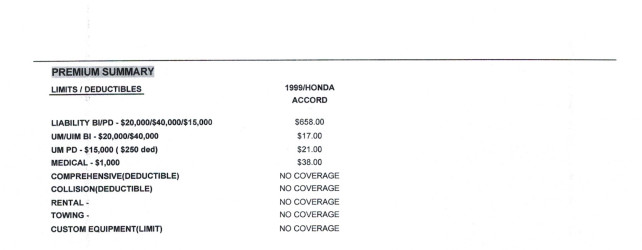

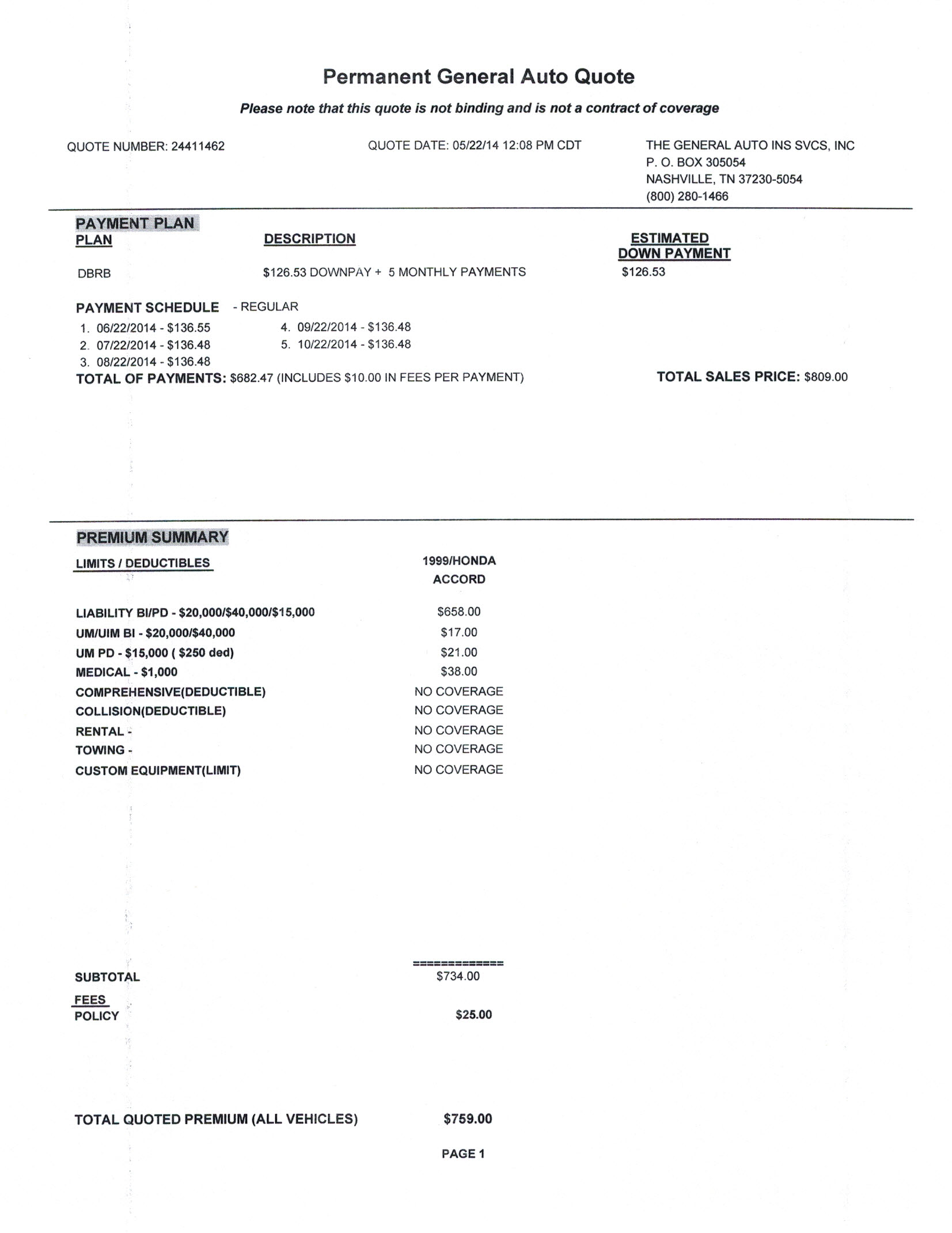

Today we had a 20 year old client with a 1999 Honda Accord. He asked us to give him a comparison rate to “The General”. We used the same coverage, vehicle and driving record.

Today we had a 20 year old client with a 1999 Honda Accord. He asked us to give him a comparison rate to “The General”. We used the same coverage, vehicle and driving record.

The result? One of our many companies will save him $375.00 per six months, or $750.00 per year.

At this point our new client says “Wait a minute, REALLY???”

Here is the proof……

Why should you choose an independent agency?

November 21, 2013 by

Some people think it doesn’t really matter where they buy their insurance. But this misconception could be costing them money, service and protection. Buying insurance isn’t like buying bread or milk. Insurance is an important safety net for your family your home, your car or your business. Don’t treat the purchase lightly!

There is a difference in where you buy your protection. Many people don’t realize there are four sources for insurance:

1. Captive Agents, who can sell you the insurance of only one company. (Farmers, State Farm, Allstate, etc.)

2. Telephone Representatives, who can offer you the insurance of one company and only on the telephone.

3. Internet sites where you can fill out an application online and get an insurance quote without any help or direction from a qualified professional.

4. Independent Insurance Agents who represent an average of eight insurance companies, and research with these firms to find you the best combination of price, coverage and service.

Your Independent Insurance Agent:

- Is a licensed professional with strong customer and community ties

- Gives you excellent service and competitive prices because your agent can access the insurance coverage form more than one company.

- Unlike other agents, is not beholden to any one company; thus, you don’t have to change agencies as your insurance and service needs change.

- Assists you when you have a claim.

- Is your consultant, working with you as you determine your needs.

- Offers you a choice of insurance plans and programs.

- Is a value hunter who looks after your wallet in finding the best combination of price, coverage and service.

- Offers one-stop shopping for a full range of products – home, renters, auto, business, life, and pretty much everything else.

- Can periodically review your coverage to keep up with your changing insurance needs.

- Treats you like a person, not just another number.

- Customer satisfaction is the key to an independent agent’s livelihood, since serving you is your independent agent’s most important concern.

Are you a Pekin Insurance orphan?

May 7, 2013 by

Recently an area agency lost it’s Pekin Insurance contract.

We have represented Pekin Insurance Company since 1955. We have the ability to move your policy(ies) to our agency with the use of a simplified form.

For more information please contact us at 217-355-5555.

Money Saving Tips and Information

April 25, 2013 by

How Can I Save Money On Auto Insurance?

The price you pay for your auto insurance can vary by hundreds of dollars, depending what type of car you have and the insurance company you buy your policy from. Here are some ways to save money.

1. LET US SHOP AROUND

Prices vary from company to company, so it pays to let us do the shoppping for you.

You buy insurance to protect you financially and provide peace of mind. Don’t shop by price alone. Ask friends and relatives for their recommendations. Pick an independent agent representative that takes the time to answer your questions.

2. BEFORE YOU BUY A CAR, COMPARE INSURANCE COSTS

Before you buy a new or used car, check into insurance costs. Car insurance premiums are based in part on the car’s price, the cost to repair it, its overall safety record and the likelihood of theft. Many insurers offer discounts for features that reduce the risk of injuries or theft. To help you decide what car to buy, you can get information from the Insurance Institute for Highway Safety (www.iihs.org).

3. ASK FOR HIGHER DEDUCTIBLES

Deductibles are what you pay before your insurance policy kicks in. By requesting higher deductibles, you can lower your costs substantially. For example, increasing your deductible from $200 to $500 could reduce your collision and comprehensive coverage cost by 15 to 30 percent. Going to a $1,000 deductible can save you 40 percent or more. Before choosing a higher deductible, be sure you have enough money set aside to pay it if you have a claim.

4. REDUCE COVERAGE ON OLDER CARS

Consider dropping collision and/or comprehensive coverages on older cars. If your car is worth less than 10 times the premium, purchasing the coverage may not be cost effective. Auto dealers and banks can tell you the worth of cars. Or you can look it up online at Kelley’s Blue Book (www.kbb.com). Review your coverage at renewal time to make sure your insurance needs haven’t changed.

5. BUY YOUR HOMEOWNERS AND AUTO COVERAGE FROM THE SAME INSURER, OR IS BUNDLING ALWAYS THE CORRECT ANSWER?

Many insurers will give you a break if you buy two or more types of insurance. You may also get a reduction if you have more than one vehicle insured with the same company. Some insurers reduce the rates for long-time customers. But it still makes sense to let us shop around! You may save money buying from different insurance companies, compared with a multipolicy discount.

6. MAINTAIN A GOOD CREDIT RECORD

Establishing a solid credit history can cut your insurance costs. Most insurers use credit information to price auto insurance policies. Research shows that people who effectively manage their credit have fewer claims. To protect your credit standing, pay your bills on time, don’t obtain more credit than you need and keep your credit balances as low as possible. Check your credit record on a regular basis and have any errors corrected promptly so that your record remains accurate.

7. TAKE ADVANTAGE OF LOW MILEAGE DISCOUNTS

Some companies offer discounts to motorists who drive a lower than average number of miles per year. Low mileage discounts can also apply to drivers who car pool to work.

8. SEEK OUT OTHER DISCOUNTS

Companies offer discounts to policyholders who have not had any accidents or moving violations for a number of years. You may also get a discount if you take a defensive driving course. If there is a young driver on the policy who is a good student, has taken a drivers education course or is away at college without a car, you may also qualify for a lower rate.

When you contact us for your quotes, inquire about discounts for the following:*

Antitheft Devices

Auto and Homeowners Coverage with the Same Company

College Students away from Home

Defensive Driving Courses

Drivers Ed Courses

Good Credit Record

Higher deductibles

Low Annual Mileage

Long-Time Customer

More than 1 car

No Accidents in 3 Years

No Moving Violations in 3 Years

Student Drivers with Good Grades